All Categories

Featured

Table of Contents

Costs are typically less than whole life plans. With a degree term policy, you can select your protection amount and the policy length. You're not locked right into a contract for the rest of your life. Throughout your policy, you never ever need to worry regarding the premium or fatality advantage amounts altering.

And you can't squander your policy during its term, so you won't obtain any type of economic gain from your previous protection. Just like other sorts of life insurance policy, the cost of a level term plan relies on your age, coverage needs, work, lifestyle and health and wellness. Generally, you'll locate extra budget friendly coverage if you're more youthful, healthier and much less risky to guarantee.

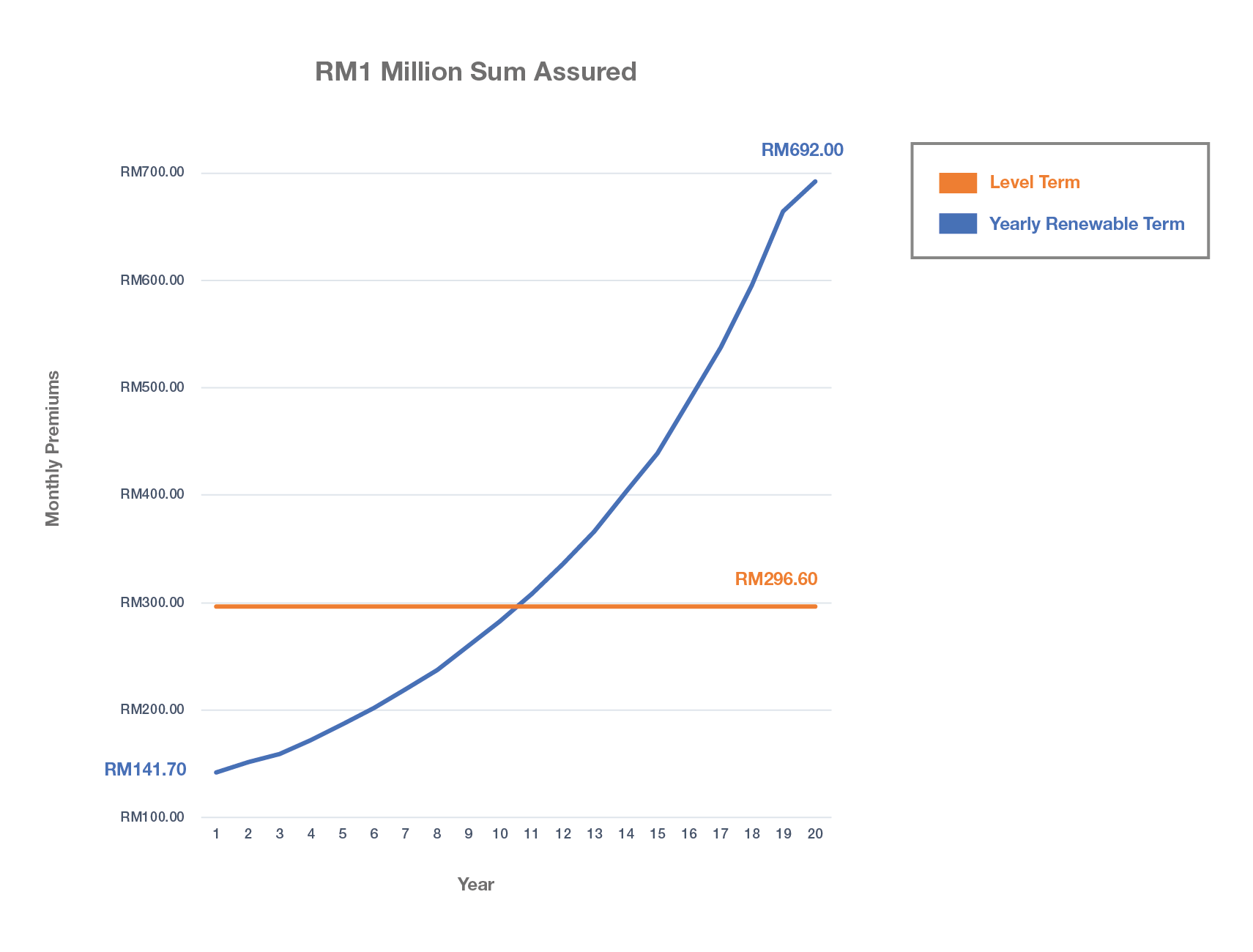

Because level term costs remain the exact same for the period of protection, you'll know exactly how much you'll pay each time. That can be a large help when budgeting your costs. Level term insurance coverage likewise has some flexibility, allowing you to tailor your policy with added features. These typically come in the kind of riders.

You might have to satisfy details problems and credentials for your insurance firm to enact this motorcyclist. There also could be an age or time restriction on the insurance coverage.

Fixed Rate Term Life Insurance

The survivor benefit is typically smaller sized, and insurance coverage normally lasts up until your child transforms 18 or 25. This rider may be a much more cost-efficient way to aid ensure your youngsters are covered as cyclists can commonly cover multiple dependents at the same time. As soon as your kid ages out of this insurance coverage, it might be feasible to transform the cyclist into a new policy.

When contrasting term versus permanent life insurance policy, it is necessary to keep in mind there are a couple of different types. One of the most common sort of irreversible life insurance is whole life insurance coverage, yet it has some crucial distinctions contrasted to degree term coverage. Right here's a fundamental summary of what to consider when comparing term vs.

:max_bytes(150000):strip_icc()/Investopedia-terms-termlife-6451fde927474d4f8a81a5681efd393f.jpg)

Whole life insurance policy lasts for life, while term insurance coverage lasts for a details period. The premiums for term life insurance policy are typically reduced than whole life coverage. With both, the premiums remain the very same for the period of the policy. Whole life insurance policy has a cash worth component, where a portion of the costs may expand tax-deferred for future requirements.

How can Term Life Insurance With Fixed Premiums protect my family?

Among the highlights of degree term insurance coverage is that your costs and your death advantage don't alter. With reducing term life insurance, your premiums remain the same; nonetheless, the death advantage quantity obtains smaller gradually. As an example, you may have coverage that starts with a survivor benefit of $10,000, which could cover a home mortgage, and then yearly, the survivor benefit will certainly decrease by a set amount or percentage.

Due to this, it's typically an extra inexpensive kind of degree term insurance coverage., but it may not be sufficient life insurance for your demands.

After deciding on a plan, finish the application. If you're authorized, sign the paperwork and pay your first costs.

You may desire to update your recipient details if you've had any kind of considerable life changes, such as a marital relationship, birth or separation. Life insurance coverage can sometimes feel complicated.

How do I apply for Affordable Level Term Life Insurance?

No, level term life insurance policy does not have money worth. Some life insurance policy policies have a financial investment function that permits you to construct cash money value in time. Level term life insurance coverage. A part of your costs payments is alloted and can earn passion gradually, which expands tax-deferred throughout the life of your insurance coverage

These policies are frequently substantially much more pricey than term coverage. You can: If you're 65 and your insurance coverage has actually run out, for example, you might want to buy a new 10-year level term life insurance coverage plan.

Level Term Life Insurance Benefits

You may be able to transform your term insurance coverage right into a whole life policy that will last for the remainder of your life. Lots of kinds of degree term policies are convertible. That suggests, at the end of your insurance coverage, you can convert some or all of your plan to whole life insurance coverage.

Level term life insurance policy is a plan that lasts a set term generally in between 10 and three decades and features a level death benefit and degree costs that remain the same for the entire time the policy is in effect. This suggests you'll recognize exactly just how much your repayments are and when you'll need to make them, allowing you to budget as necessary.

Level term can be an excellent alternative if you're wanting to acquire life insurance policy protection for the very first time. According to LIMRA's 2023 Insurance coverage Barometer Study, 30% of all adults in the U.S (20-year level term life insurance). requirement life insurance and don't have any type of kind of plan. Degree term life is predictable and budget friendly, which makes it one of the most popular types of life insurance policy

A 30-year-old male with a similar account can expect to pay $29 per month for the very same protection. AgeGender$250,000 insurance coverage amount$500,000 protection quantity$1 million protection amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Method: Average regular monthly prices are computed for male and female non-smokers in a Preferred wellness classification getting a 20-year $250,000, $500,000, or $1,000,000 term life insurance policy plan.

Is there a budget-friendly 30-year Level Term Life Insurance option?

Prices might vary by insurer, term, insurance coverage amount, health class, and state. Not all plans are offered in all states. Rate picture valid as of 09/01/2024. It's the cheapest type of life insurance policy for many people. Level term life is much extra inexpensive than a similar entire life insurance policy plan. It's easy to handle.

It permits you to spending plan and prepare for the future. You can easily factor your life insurance coverage right into your spending plan because the premiums never transform. You can prepare for the future simply as conveniently because you understand specifically just how much cash your loved ones will receive in the occasion of your absence.

How much does Level Term Life Insurance cost?

In these instances, you'll generally have to go via a brand-new application process to get a better rate. If you still need coverage by the time your level term life policy nears the expiration day, you have a couple of choices.

{kind=link}

Latest Posts

Low Cost Burial Insurance

Funeral Life Insurance Policy

What Is The Difference Between Life Insurance And Final Expense